A retenir

- You may be held criminally liable in the event of a customs inspection.

- The authorities carry out an automated risk analysis of the value, origin and code of the goods for each operation.

- Poor management of suspended procedures carries a high risk of adjustment and financial penalties.

- Anticipating these risks with a compliance audit helps to avoid any infringements during international transport.

- Goldwin Avocats protects your rights and ensures that every customs visit goes smoothly.

An unforeseen customs inspection can paralyse your business and make you criminally liable as a manager, up to and including indictment, depending on the seriousness of the offence. This article details each type of procedure, how company inspections are carried out and the regulations relating to the value of your goods. By mastering these keys, you can reduce the risk of adjustment and ensure that your international trade complies with the authorities. Take advantage of a defence strategy with a customs lawyer in Paris to protect your cash flow against any fines or heavy penalties. To react correctly, it is crucial to understand and anticipate customs intervention.

Guide to customs inspections: how to anticipate customs intervention

Customs control is a cornerstone of every country’s trade policy for regulating the flow of goods.

Types of customs control: from physical inspection to accounting audit

The customs administration has several means at its disposal to carry out its mission of combating fraud and ensuring the security of international trade:

- immediate controls are carried out at the time of customs clearance, often at the port or airport, to check the immediate conformity of the goods.

- Delayed inspection: more common for professionals, this takes place after the goods have been released, allowing the officer to check the documents without blocking transport.

- a posteriori control: this takes the form of a full audit of the stock accounts covering the last 3 years for national taxes, 5 years for customs duties within the meaning of the CDU (Union Customs Code), and up to 6 years in the case of customs offences. This lengthy procedure scrutinises your entire international strategy and your compliance with the chosen customs regime.

Customs inspection on your premises: the stages of the on-site visit

The inspection process generally begins with an official notification, although the authorities may intervene unannounced.

The authorised official arrives at the head office or logistics site to begin the investigation phase.

The staff must be able to connect the agents to the information systems so that the declaration data can be extracted. During the day, agents conduct interviews to understand the internal processes involved in implementing operations. Investigative powers include copying digital files and seizing original documents if an offence is suspected.

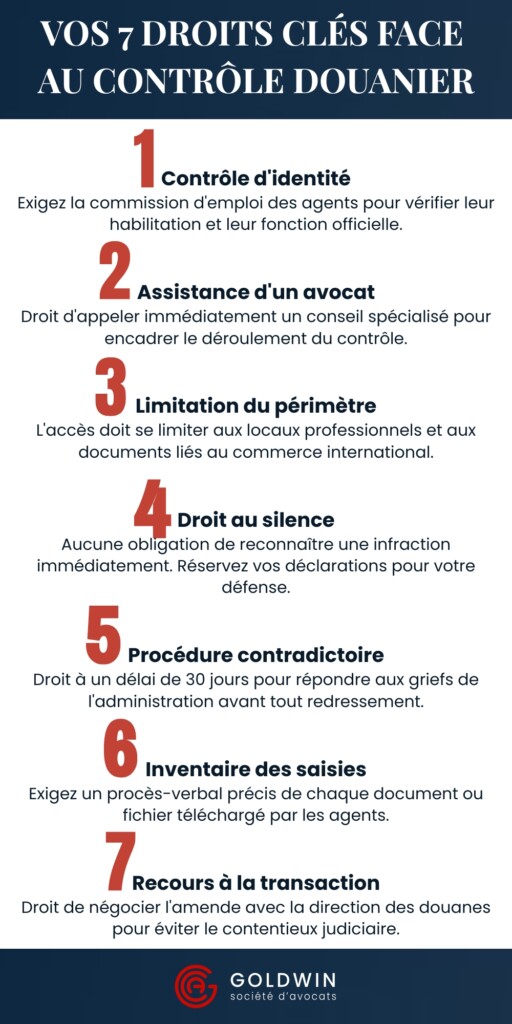

- Reflex 1: check the identity and clearance of each agent present.

- Reflex 2 : prepare a dedicated workspace to isolate the administration.

- Reflex 3 : designate a single point of contact specialising in customs law.

Objects of the inspection: verification of products, value and origin

The central objective for customs is to check that each product declared corresponds to the physical and accounting reality.

Three pillars are systematically examined:

- the tariff species (HS code),

- value

- origin.

An error in classification can lead to a massive customs adjustment if the quantity of goods imported is large. Origin is also a European economic protection issue. The customs service particularly tracks down false declarations of origin aimed at circumventing trade defence measures.

| Critical document | Main function for the customs officer | Compliance checkpoint |

|---|---|---|

| Customs declaration (H7 or H1) | Legal document identifying the customs procedure applicable to the operation. | Strict concordance between the declared procedure and the actual nature of the flow. |

| Commercial invoice | Basis for calculating customs duties. | Risk of reassessment of value by the authorities in accordance with the EU Customs Code if inconsistent. |

| Transport document (LTA / CMR) | Proof of the physical movement of the goods and their origin. | A simple error in gross weight can trigger immediate suspicion of substitution of goods. |

| Proof of origin (Certificate) | To justify the application of a preferential customs duty or trade measure. | Production is only required in certain specific situations, depending on the customs procedure. |

| Import permits | Prior authorisation for products subject to specific regulations. | Check the validity of the licence before presenting the goods to customs. |

| MACF certificates | Proof of compliance with the Border Carbon Adjustment Mechanism, which entered its definitive phase on 1 January 2026. | Declaration requirement for carbon-intensive products, subject to penalties. |

| Packing list | Precise details of the contents of each package to facilitate the physical inspection of goods. | Any discrepancy between the list and the actual contents may result in the goods being detained. |

If you are subject to an unannounced visit, contact a lawyer in Paris immediately to ensure that your interests are protected.

Infringements and misrepresentations: the financial risks for companies

A simple data entry error can turn into a serious customs offence under French law.

Lack of documents and obstruction: the pitfalls of the procedure

Lack of documentary preparation is the first source of friction during a customs inspection of a company.

If a logistics manager cannot produce the required supporting documents, the officer may suspect deliberate fraud. Any action perceived as a means of slowing down access to information is classed as obstructing the performance of duties. This offence is subject to a specific fine and may aggravate the penalties associated with the main dispute. It is therefore useful to have a clear internal procedure page for each employee involved in international transport.

Lack of internal compliance and poor management of customs procedures

The use of specific customs procedures (suspended procedures) within the company requires unfailing organisational rigour to avoid any reclassification by the authorities.

Whether it’s inward processing for transformation, customs warehousing for storage or temporary admission, these duty and tax suspension mechanisms are fragile levers of competitiveness.

The major risk lies in the disconnect between the actual logistics flows and the accounting entries sent to customs. Poor management of clearance times or a carry-over error in the import VAT reverse charge is enough to turn a financial advantage into an immediate customs adjustment.

A faulty internal procedure exposes the logistics manager to automatic penalties as soon as the traceability of goods is no longer guaranteed.

| Customs procedure | Main use | Financial advantage | Points to watch (Risks) |

|---|---|---|---|

| Release for consumption |

Final importation | Free disposal of goods | VAT reverse charge error and incorrect tariff classification. |

| Customs warehouse | Long-term storage | Unlimited suspension of duties and taxes | Traceability: disconnection between physical stocks and accounting entries. |

| Active upgrading | Transformation / Repair | No customs duties on imported components | Discharge: non-compliance with re-export deadlines for finished products. |

| Passive processing | Processing abroad | Taxation only on added value | Proof of origin and complexity of calculating customs value on return. |

| Temporary admission | Exhibition / Professional equipment | Total or partial exemption | Improper use: use outside the intended scope or exceeding deadlines. |

| Transit (T1 / T2) | Transport between zones | Smooth logistics flows | Non-discharge: risk of joint payment of duties if the journey is not completed. |

| Free zones | Storage / Processing outside customs territory | Total suspension of duties and taxes during the stay | Compliance: tighter controls and risk of reclassification as release for consumption. |

Goldwin Avocats can help you audit your processes and ensure compliance with the obligations associated with each type of regime, in order to safeguard your professional status.

Your rights and remedies: the role of a customs lawyer

Calling on the services of a lawyer is an essential protective measure against the powers of the authorities.

The right to legal counsel and the principles of adversarial proceedings

All company directors have the right to be assisted by a person of their choice during the audit.

At the end of the investigations, if any breaches are found, the authorities must follow an adversarial procedure. You will receive notification of the infringement, to which you will have an average of 30 days to respond with your observations. It is during this phase that the customs lawyer plays a crucial role by drafting a technical brief to challenge the classification of the facts. This stage is compulsory before any recovery action or prosecution before the public prosecutor.

A Goldwin Avocats lawyer is available to advise you in real time during your customs inspection.

Settling with the authorities: negotiating fines and avoiding litigation

Settlement is often the most effective way of bringing a customs adjustment case to a close.

It allows the company to acknowledge the offence in exchange for a significant reduction in the fine. The specialist firm analyses the mitigation criteria: absence of illicit traffic, manifest good faith or material error. This negotiation with the customs authorities avoids a public trial and ensures the legal security of the structure.

If a settlement is refused, the dispute may be referred to the criminal court (criminal aspect) or the administrative court (tax aspect), with the possibility of a preliminary reference to the Court of Justice of the European Union on questions of interpretation of European law.

The customs compliance audit: securing your flows before the inspection

In the context of the 2026 reform, customs compliance requires a complete overhaul of nomenclatures, declaration flows, contracts with forwarding agents and MACF obligations.

6 steps to anticipate customs controls

Compliance audit: securing your flows before inspection

A preventive customs compliance audit begins with an inventory of the procedures used and verification of tariff nomenclatures (HS6). This approach, which is essential for preparing for a customs inspection, identifies systemic errors likely to attract the attention of the Directorate General of Customs during a deferred inspection.

The audit results in a remediation plan that distinguishes between immediate risks and structural issues.

By spontaneously updating your practices, you can avoid fines and adjustments to your international trade operations. This specialised service simulates a risk analysis identical to that carried out by the authorities, whether your flows pass through a port, a railway station, an airport or a border. You get the control advice you need to secure the value of each product going to any foreign country.

Frequently asked questions about customs controls

- Reservations: essential, as the penalty notice is authentic until proven otherwise (Art. 336 of the Customs Code).

- Appeals: you can refer disputes of value/origin to the Regional Director or the SEAC.

- Legal proceedings: only the courts have jurisdiction to challenge the validity of the penalty notice.

- Settlement: under article 350, the public prosecution is extinguished, but the offence is acknowledged.

- Time limit: generally 2 months for an administrative appeal.