A retenir

- Voluntary liquidation is a voluntary procedure reserved for companies that have not suspended payments.

- This procedure assumes that the company’s available assets are sufficient to repay all debts and creditors in full.

- A poorly managed early winding-up makes the director personally liable for any unknown liabilities.

- The liquidation process requires a general meeting, a legal announcement, and a file submitted to the one-stop shop.

- The company is finally struck off the register of companies only after the liquidation has been completed and the company has been discharged.

Whether you are the manager of a SARL or EURL, or the chairman of an SAS, ceasing trading due to retirement or the end of a joint project is not something you can improvise. If the company is not wound up properly, you could be personally liable to creditors or the tax authorities. This comprehensive guide details every stage in the voluntary winding-up process , from the general meeting at which the company is wound up to the final deletion from the national register of companies via the one-stop shop. You will learn how to manage the liquidation process to avoid errors in social security declarations, secure liabilities andoptimise the calculation of bonuses.

To ensure the success of your voluntary approach, let’s first look at why voluntary liquidation is a preferred procedure for orderly closure.

Definition and conditions of voluntary liquidation: why choose the voluntary route?

Voluntary liquidation is a procedure that enables a legal entity to be wound up without going to commercial court in a conflictual manner. Unlike a forced closure, it is based on the will of the partners. It assumes that the company has sufficient available assets to repay the liabilities that are due and payable. This is the ideal option for managers wishing to control the timetable for ceasing trading while protecting their professional image.

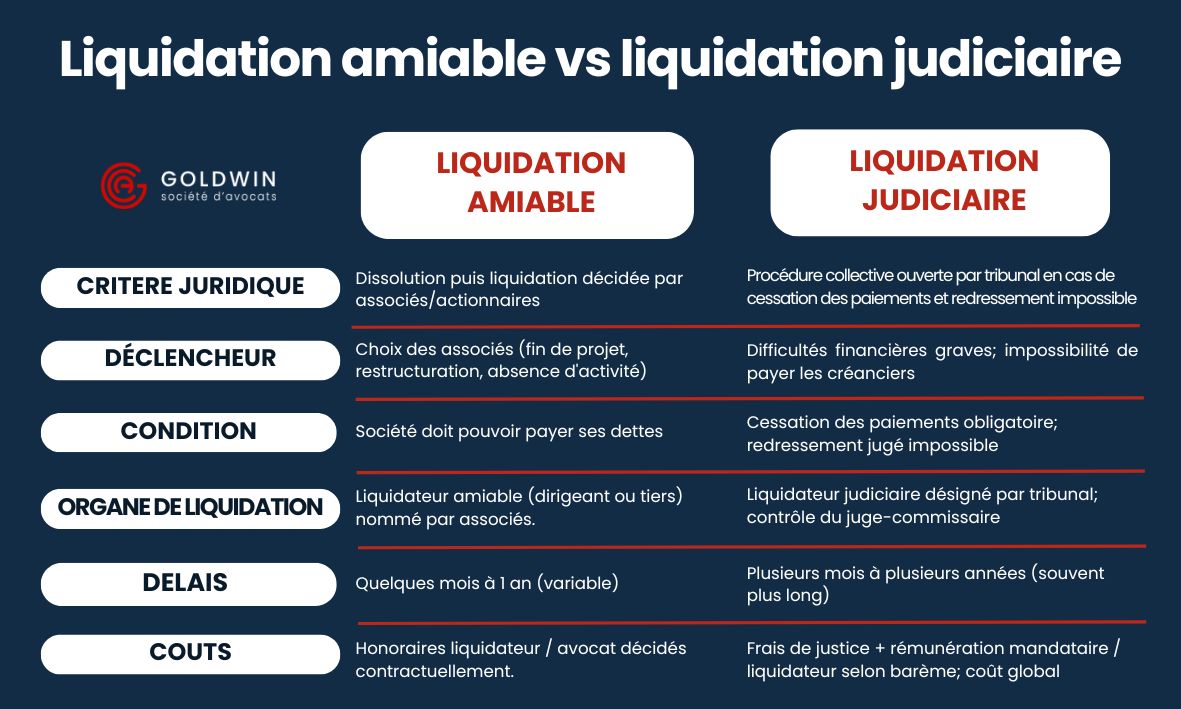

Difference between voluntary and judicial liquidation: what impact for the manager?

The major distinction lies in the notion of control and cost. In voluntary liquidation, you appoint your own liquidator, often yourself or a trusted professional, whereas in compulsory liquidation, the Commercial Court (traders and companies) or the Court of First Instance (non-trading companies, associations or the liberal professions) appoints a judicial representative. These collective proceedings are necessary as soon as it is clear that payments have ceased. For managers, voluntary proceedings avoid the stigma attached to financial difficulties and allow for more flexible management of liquidation operations.

The absence of cessation of payments: a condition for voluntary dissolution

Voluntary liquidation is prohibited in the event of suspension of payments. You must be able to repay all your liabilities (due and payable). If your assets are insufficient, you have 45 days in which to declare the cessation of payments to the court.

Warning:

Forcing a voluntary liquidation when the company is insolvent constitutes serious mismanagement, exposing the director to an action to make good the company’s liabilities using his or her personal assets.

To validate your eligibility, check the following points:

- No unpaidtax or social security debts without a deferment agreement.

- Sufficient cash flow to cover outstanding supplier invoices.

- Ability to liquidate stocks or equipment to settle accounts.

- Unanimous or majority agreement of the partners, depending on the articles of association.

Advantages and reasons for voluntary dissolution

Voluntary dissolution is much more than a simple administrative formality: it is a strategic decision that allows you to close a professional chapter while protecting your assets. In contrast to procedures that have to be followed, voluntary dissolution offers the company director the luxury of time and financial control.

A variety of reasons adapted to business life

In addition to the end of a business activity, there are a number of other situations in which shareholders may vote to dissolve the company early:

- Retirement or a change of life: The company director wishes to step down without having found a buyer for his shares. Liquidation enables him to recover his contributions and accumulated reserves.

- The end of a joint project or disagreement: Partners who no longer share the same vision may decide to wind up the company and “go their separate ways”, thus avoiding a prolonged management deadlock.

- Fulfilment of the company’s objects: A company set up specifically for a property project or the production of a specific event no longer has any reason to exist once the mission has been accomplished.

- Group simplification: As part of a restructuring, a parent company may decide to wind up a subsidiary that has become inactive in order to simplify its legal structure.

MOTHBALLING

Mothballing temporarily suspends activity without dissolving it. Ideal for a pause of no more than 2 years, this option maintains the company’s legal personality.

Please note: it does not exempt you from your legal obligations. You must declare the temporary cessation to the RCS and continue to file your tax returns. This is a reversible alternative to permanent closure, and is useful before deciding whether to liquidate or take over.

The practical benefits of an orderly exit

Opting for this route offers substantial advantages that cannot be found in other closure methods:

- Recurring savings : Maintaining an “empty shell” is expensive. Between the Cotisation Foncière des Entreprises (CFE), bank account maintenance fees, chartered accountant fees for annual balance sheets and legal secretarial fees, the bill can run to several thousand euros a year for an inactive company.

- Recovery of assets (Bonus): If the company has been soundly managed, the liquidation will generate a bonus. This is when the partners get back their tax-free initial investment (share capital), as well as the surplus profits placed in reserve, which are often taxed more favourably than traditional salaries.

- Legal certainty and “social peace”: By carrying out an official liquidation with legal publicity, you trigger the limitation periods. This allows you to purge your liabilities and avoid creditors turning up years later when you have already turned the page.

- Freedom of management: As the appointed liquidator, you decide for yourself how to sell your assets (equipment, stock, vehicles). You are not subject to forced auction, which maximises the exit value.

Step 1: How do you successfully dissolve your company early?

The dissolution of the company is the legal act that initiates its closure. Although commercial activity ceases, the legal personality survives for the purposes of liquidation. This is a transitional period during which the registered office often remains the same, but the legal representative changes title.

At this stage, the slightest drafting error in your legal documents or an omission in the minutes can block your file at the Registrar’s office and result in heavy tax penalties.

The Extraordinary General Meeting (EGM) and appointment of the liquidator

It all starts with an Extraordinary General Meeting. The shareholders vote to dissolve the company and appoint a liquidator. Minutes of the dissolution must be drawn up in detail, setting out the end of the executive’s term of office and the scope of the new representative’s powers. The liquidator may be theformer director, a partner or a third party professional, provided thereis no conflict of interest in the case of regulated professions. This document is the centrepiece of the liquidation file filed at a later date.

To ensure legal certainty at this stage and protect your personal assets, it is essential to work with GOLDWIN AVOCATS, Paris 16, experts in company law. It will ensure that your decisions are valid in the eyes of third parties and guarantee a smooth transition to deregistration.

Filing formalities with the Guichet Unique and publication notices (JAL) in 2026

Once the deed has been signed, you must publish a legal notice in an official newspaper in your département within 30 days. This announcement informs third parties and any creditors of the company’s situation. Once this has been done, the application must be sent electronically to the one-stop shop managed by INPI. This service centralises the application for the clerk’s office of the commercial court and the trade and companies register (RCS).

For your application to be validated without rejection by the commercial court clerk’s office, you must attach the following documents:

- A copy of the dissolution minutes, certified as true by the liquidator.

- Acertificate of publication in a legal gazette (JAL).

- A declaration of non-conviction and a certificate of filiation from the liquidator.

- A copy of the representative’s valid identity card or passport.

- The updated RBE form (Register of Beneficial Owners) if the dissolution results in a change at this level.

Stage 2: The liquidation process and the role of the liquidator

Once the company has been dissolved, the liquidation phase begins. This is where the real work begins. The liquidator’s task is to empty the company of its financial substance in preparation for its final closure. He becomes the only legal representative able to act on behalf of the legal entity. Any error in the management of assets or the repayment of debts at this stage is tantamount to incurring civil liability.

What are the roles and tasks of the liquidator when the assets are realised?

The liquidator must realise the assets, i.e. sell the furniture and stock and collect all customer debts. With the funds collected, he must repay the creditors in order of priority: employees, tax authorities, social security bodies, then suppliers. He must also draw up a liquidation report detailing all the liquidation operations carried out.

This report will be presented to the partners at the final closing to obtain their discharge.

NOTES

The legal personality survives only for the purposes of the closure. The company continues to act in its own name, but you must add the words “Company in liquidation” and the name of the liquidator to all your documents (invoices, letters, advertisements). Failure to comply with this legal obligation may result in criminal penalties.

Controlling the partners and the role of the CSE

Even if the liquidator has his hands on the wheel, the shareholders retain a power of control over the liquidation process. They must be kept informed of progress at least once a year if the procedure is to continue.

In addition, if the company employs staff, the CSE (Comité Social et Économique) must be consulted. Labour law requires these stages of social dialogue to be respected, otherwise the procedure may be challenged in the courts.

Closure of liquidation operations: obtaining removal from the Kbis register

Closing the liquidation is the final stage. It is the moment when it is established that everything has been sold and paid for. A final general meeting is called to approve the liquidation accounts.

To ensure that these final documents are in order, consulting a specialist lawyer from the GOLDWIN AVOCATS business law firm in Paris 16 is a useful precaution toavoid any rejection by the court clerk’s office.

Closing accounts, discharge of the liquidator and calculation of the liquidation surplus

The liquidator presents the final accounts. If the proceeds from the realisation of assets are greater than the repayment of liabilities and share capital, a liquidation surplus is recorded. This amount belongs to the shareholders but is subject to specific taxation (flat tax or scale).

The shareholders vote to discharge the liquidator from his duties. If the balance is negative, it is referred to as a deficit, and the shareholders lose their initial investment without being able to be sued for the surplus debts (except in the case of mismanagement).

ATTENTION

Never leave unpaid debts to run. It is essential to anticipate the balance of your tax and social security obligations (VAT, Urssaf) and the termination of your lease and current contracts before the accounts are closed. Rigorous management of liabilities is essential to protect your personal liability and avoid any disputes after deregistration.

Deregistration formalities and legal deadlines

The final file is submitted to the one-stop shop to have the company struck off the register of companies. The liquidation period is generally a few months, but the law requires that it should not exceed three years without renewal. Once the company has been struck off the register, you will receive a K-bis extract stating that the liquidation has been completed.

This document is the official proof that thecompany no longer exists legally.

Support strategy: Optimising costs and security

The cost of an voluntary liquidation varies depending on whether you take the necessary steps alone or with a professional. Between the costs of legal announcements, registry fees and honoraria, the budget can quickly climb. However, there is a real risk of being held liable by a forgotten creditor. Choosing the right support solution is therefore as much a financial decision as a strategic one for the business owner.

To make this stage as secure as possible, the choice between independent management and using the services of a specialist firm depends on the complexity of your liabilities. A case involving real estate assets or patents requires specialised legal expertise to avoid any subsequent administrative blockage.

Advanced risks and opportunities: what nobody tells you about liquidation

Beyond the official forms, certain aspects of the closure process are often ignored. Yet these grey areas can represent significant financial value or hidden risks.

Managing intangible assets: trademarks, domain names and data

In a digital economy, a company’s value is not limited to its stock or furniture. Intangible assets are often the most neglected when the liquidation report is drawn up, even though they represent tangible financial value.

- Trademarks and patents: If your trademark has a certain reputation, the liquidator should value it. It may be sold to a third party or allocated to a partner at the time of division.

ATTENTION

Once the company has been struck off the register, its legal personality disappears. Without a prior deed of assignment, the trademark becomes “property without a master”, making any subsequent use or sale legally perilous.

- Domain names and data: Your customer file (RGPD compatible) and your domain name have a market value. The liquidator must organise the technical and legal transfer of these properties.

The value of these transfers increases the liquidation proceeds and, by extension, the bonus distributable to the shareholders.

Survival of liability after deregistration: unknown liabilities

Deregistration from the Trade and Companies Register (RCS) marks the end of commercial life, but not necessarily the end of legal risk. The principle is clear: a company’s legal personality survives as long as its rights and obligations have not been liquidated.

- The ad hoc representative: A “forgotten” creditor (supplier, former employee or tax authorities) may apply to the President of the Court for the appointment of an ad hoc representative. The latter’s task will be to represent the company, even though it has been struck off the register, in order to claim payment of a debt.

- The liquidator’s liability: If the liquidator was aware of the existence of a dispute or an unfunded debt, he or she may be held personally liable. He may be ordered to pay the debt out of his own funds.

EXPERT ADVICE

Insist on a certificate of tax and social security regularity (Urssaf) and make sure that no formal notice has gone unanswered before signing the closing minutes.

Voluntary liquidation and transfer: can an “empty shell” be sold?

Before going into liquidation, it is essential to compare the cost of liquidation with the opportunity to sell the legal structure. A “clean” (debt-free) company may have intrinsic value for a buyer.

- History and track record: A company that has been in existence for 10 years is often better perceived by banks than a new structure. A buyer might be prepared to buy your “empty shell” simply to benefit from this history and its already paid-up share capital.

- Approvals and licences: Certain administrative approvals or operating licences are attached to the legal entity. Winding up the company means destroying these assets. A sale of shares enables these valuable rights to be transferred.

- TUP (Transmission Universelle du Patrimoine): If your company is owned by another legal entity (parent company), TUP is an alternative to traditional liquidation. It allows the subsidiary to be dissolved without liquidation, by transferring all its assets and liabilities to the parent company, thereby drastically simplifying the formalities.

To help you navigate these complex waters, the support of the GOLDWIN AVOCATS business law firm in Paris 16 secures your strategic assets during the final phase.

Closing to bounce back: the importance of a controlled voluntary liquidation

A successful voluntary liquidation is more than just filling out forms: it is the art of steering an orderly exit to protect your assets. From the early dissolution approved by the general meeting to the closing of the final liquidation, each stage requires absolute rigour to avoid any personal liability. You will now be familiar with the role of the liquidator, the formalities of the one-stop shop and the tax subtleties of the liquidation bonus.

However, between the legal deadlines and the management of liabilities, the risk of error remains real. To ensure that the process of winding up your business is a seamless transition, the support of an expert is your best guarantee.

Goldwin Avocats secures your deregistration and preserves your assets. Don’t let legal uncertainty compromise your future plans: contact us for a dedicated consultation.

Frequently asked questions about voluntary liquidation